What drives LRT yield today

Liquid Restaking Tokens (LRTs) generate returns through two distinct layers. The first layer is the base staking reward from securing the Ethereum network. The second layer comes from fees and incentives paid by Active Validation Services (AVSs) that use the restaked security. Understanding this split is the foundation of any LRT yield analysis.

Base staking rewards

The baseline for any LRT is the yield from Ethereum staking. When you stake ETH, you earn rewards for proposing and validating blocks. LRT protocols capture this yield and issue a liquid token representing your position. This base yield is relatively predictable, tied directly to Ethereum network activity and validator performance. It serves as the floor for the protocol’s total return.

AVS fees and incentives

Beyond the base layer, LRTs offer additional yield from AVSs. These are external services that rent security from the restaked ETH. Protocols like EigenLayer allow validators to opt-in to securing these services. In return, AVSs pay fees to the validators. These fees can come in various forms, including ETH, stablecoins, or the AVS’s native token. This secondary layer is where the "restaking" premium comes from, but it also introduces variable and often uncertain returns.

The yield trade-off

The total yield of an LRT is the sum of these two components. While the base staking reward is consistent, the AVS fee component fluctuates based on demand for security and the specific incentives offered by each AVS. This variability is a core part of the risk profile. Higher yields often signal higher exposure to volatile AVS tokens or less proven security services. Investors must weigh the potential for extra return against the complexity and risk of the underlying AVSs.

Protocol comparison: yield and risk

LRT Yield analysis requires evaluating how each protocol structures its return streams and where those returns break down under stress. Unlike standard liquid staking, which exposes users only to base-layer slashing, liquid restaking compounds risk. As assets secure multiple external services simultaneously, they inherit the unique slashing conditions of every individual service they validate [src-serp-5]. This structural difference means yield is not uniform; it is a direct function of the risk layers a protocol layers on top of Ethereum’s base security.

To compare these tradeoffs, we evaluate major LRT protocols across three dimensions: the source of their yield, their specific slashing exposure, and their current market size as a proxy for network health. The table below outlines the core differences between leading solutions.

| Protocol | Primary Yield Source | Slashing Risk Profile | TVL Category |

|---|---|---|---|

| EigenLayer (EIGEN) | Restaking points & incentives | Full restaking exposure | Large |

| Ether.fi (ezETH) | Staking + Restaking + DeFi | Compositional/Full | Large |

| Renzo (EZ) | Staking + Restaking | Compositional/Full | Medium |

| Puffer (PufETH) | Staking + Puffer Vault | Mitigated (Insurance) | Medium |

| Karak (K) | Restaking incentives | Full restaking exposure | Small |

The yield mechanisms vary significantly. EigenLayer and Karak rely heavily on direct restaking incentives, which can be volatile and dependent on new protocol launches. Ether.fi and Renzo offer a more diversified yield mix by integrating restaking rewards with broader DeFi strategies, potentially smoothing returns but increasing smart contract complexity. Puffer distinguishes itself by attempting to mitigate slashing risk through insurance mechanisms, offering a different risk-adjusted return profile.

Slashing risk remains the primary differentiator. In a standard LRT model, a single misbehavior can slash the entire position. Protocols like Puffer introduce insurance funds to cover these losses, effectively transferring risk from the user to the protocol’s treasury. This safety net comes at a cost, often reducing net yield compared to pure restaking protocols that pass all risk directly to the holder.

Understanding these distinctions is critical for LRT Yield analysis. Investors must decide whether they prioritize higher, riskier yields from pure restaking protocols or more stable, diversified yields from composite LRTs that manage slashing exposure.

Infrastructure risks in restaking

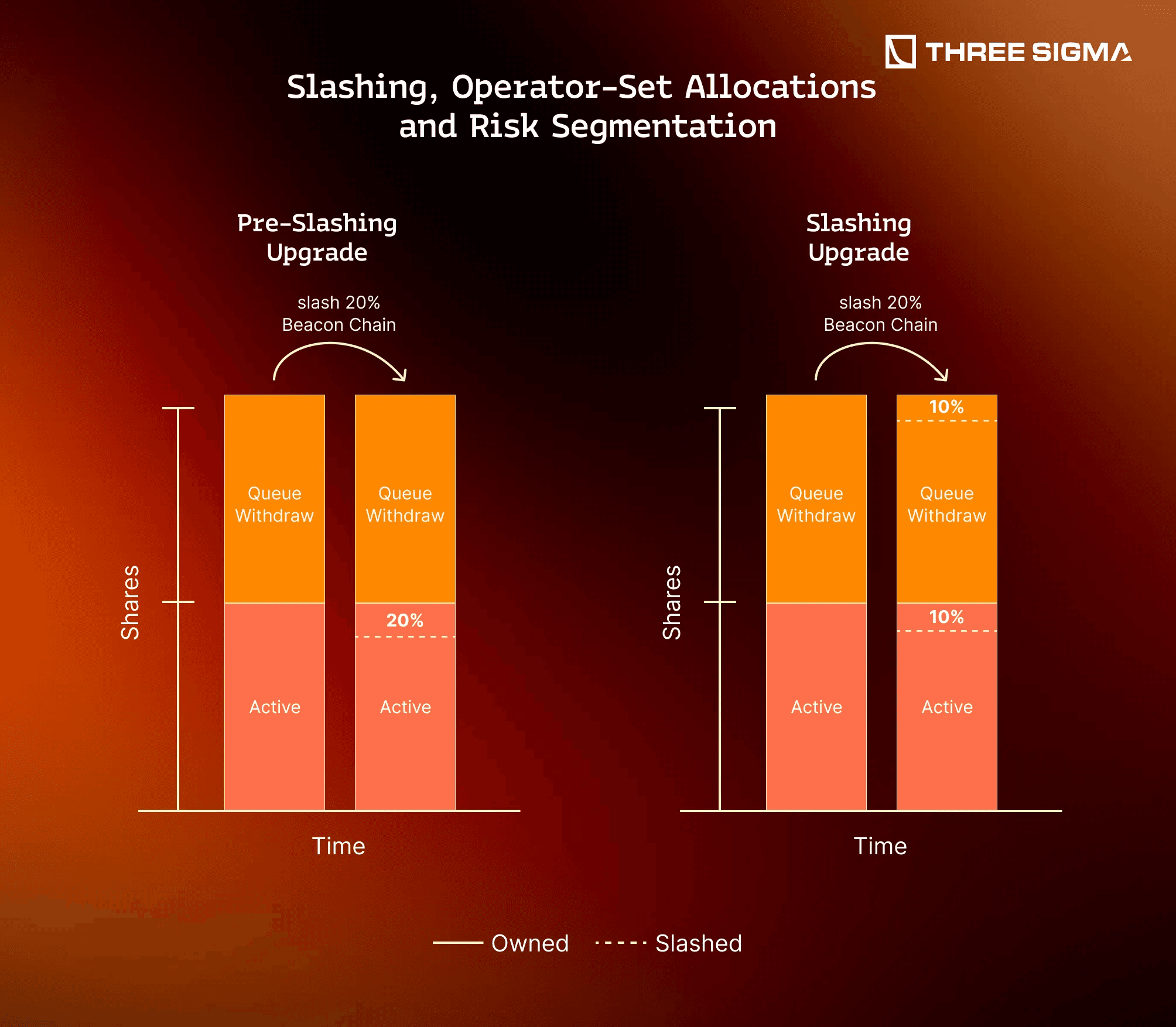

While LRT yield analysis often focuses on tokenomics and reward rates, the underlying infrastructure introduces distinct technical hazards. Liquid restaking protocols are not merely passive yield aggregators; they are complex financial machines that layer multiple smart contracts atop one another. This architectural depth creates a risk profile that diverges sharply from traditional liquid staking.

The most significant structural vulnerability is compounded slashing risk. In standard liquid staking, your assets face the base network’s slashing conditions. In liquid restaking, however, those same assets are simultaneously delegated to multiple Active Validation Services (AVSs). Each AVS operates under its own set of rules and security requirements. If an LRT provider fails to meet the specific criteria of even one integrated service, the entire restaked position can be slashed. This means a single protocol failure can trigger penalties across the whole portfolio, multiplying the exposure beyond the base layer.

Beyond slashing, smart contract complexity creates a larger attack surface. Each additional protocol integrated into the restaking stack introduces new codebases, new upgrade mechanisms, and new potential points of failure. Unlike simple staking contracts that have been battle-tested for years, LRT infrastructure often involves novel tokenomics and cross-protocol interactions that have not yet undergone extensive real-world stress testing. This complexity makes it difficult for users to audit the true safety of their capital.

To understand the current market state of these protocols, it is helpful to observe their price action and volume, which often reflect market sentiment toward these structural risks.

Liquidity and market depth

Liquidity determines how easily you can enter or exit an LRT position without moving the price. In deep pools, large trades have minimal slippage. In thin markets, even modest sell pressure can trigger sharp price drops, eroding the yield advantage.

DEX concentration is a primary risk factor. Many LRT pairs are dominated by a single automated market maker (AMM) or a few large liquidity providers. If that pool dries up or the provider withdraws capital, the token becomes illiquid. This concentration creates a fragility that simple yield charts do not show.

Whale activity further distorts market depth. Large holders can withdraw significant liquidity or execute large sell orders that exceed the available order book depth. During market stress, these actors often exit first, leaving smaller investors with reduced liquidity and higher slippage costs.

Choosing an LRT strategy

Selecting the right Liquid Restaking Token (LRT) requires aligning protocol mechanics with your personal risk tolerance and yield targets. Because LRT Yield analysis reveals that returns are not guaranteed but derived from variable AVS fees and token emissions, a structured evaluation is necessary.

Restaking compounds risk by securing multiple services simultaneously. Evaluate whether the protocol offers insurance funds or slashing protection mechanisms. Protocols with robust risk management frameworks, such as those detailed by Gauntlet, typically offer lower but more stable yields compared to those without such safeguards.

LRT returns often come from a mix of ETH staking rewards, AVS fees, and protocol-specific token emissions. Distinguish between sustainable yield from network fees and inflationary yield from token distribution. Protocols relying heavily on emissions may see yield decay as token supply increases, impacting long-term LRT Yield analysis outcomes.

High yield is irrelevant if you cannot exit the position. Review the depth of liquidity pools and the ease of swapping your LRT for underlying ETH or stablecoins. Thin liquidity can lead to significant slippage during market volatility, making exit strategies a critical component of your LRT strategy.

| Protocol | Risk Level | Primary Yield Source |

|---|---|---|

| Ether.fi | Medium | AVS Fees + eETH |

| Renzo | Medium-High | ezETH + Incentives |

| Puffer | Low-Medium | PufETH + Insurance |

Lrt yield analysis: frequently asked: what to check next

What is an LRT?

In the context of crypto yield, an LRT stands for Liquid Restaking Token. It is a liquid representation of a restaking position. While the term is also used for light-rail transit, this article focuses on the financial instrument that allows users who have staked their tokens to extend the security of the base network to other protocols and networks. This extension creates a new asset class for LRT yield analysis.

What is the difference between LST and LRT?

The primary difference lies in the source of yield and the risk profile. An LST (Liquid Staking Token) yields the base network's staking rewards. An LRT yields those base rewards plus additional rewards from each integrated protocol (the AVSs). This additional yield comes with compounded risks. Liquid staking carries standard smart contract and base layer slashing risk. Liquid restaking introduces exposure to the unique slashing conditions of every individual service the asset validates.

How do LRTs boost yield?

LRT holders can boost their yield by participating in the restaking ecosystem. This mechanism allows users to speculate on the value of points accredited by LRT protocols and implement versatile yield token strategies. By restaking, investors can capture multiple layers of rewards simultaneously, making LRT yield analysis essential for understanding the true return on investment versus the associated security tradeoffs.

No comments yet. Be the first to share your thoughts!