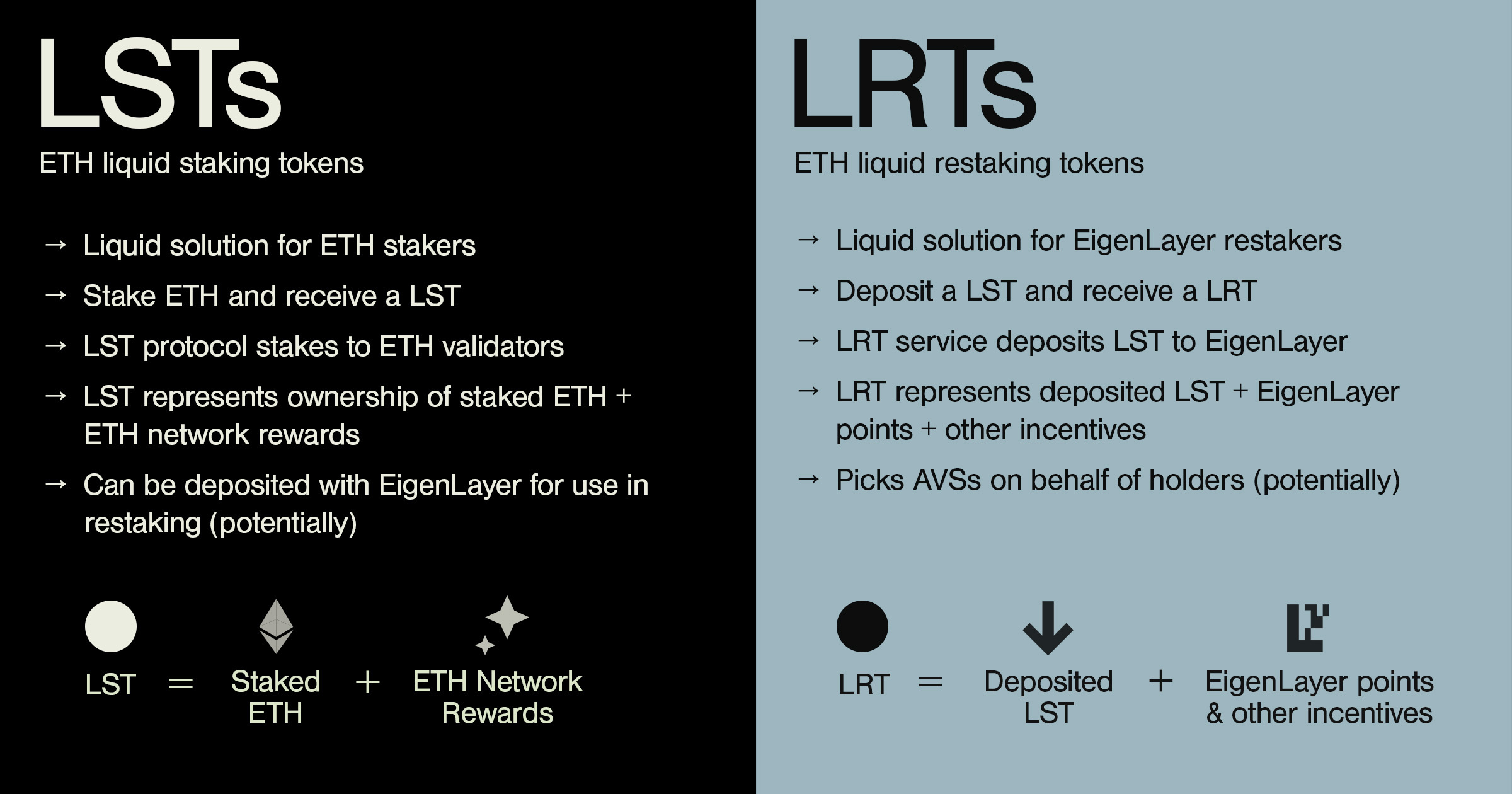

Deconstructing the LRT yield stack

To understand where LRT returns actually come from, you have to look past the headline APY. Yield is not a monolithic number; it is a composite of multiple risk vectors stacked on top of one another. Think of an LRT yield like a layered cake: each tier adds flavor (return) but also introduces new structural risks that must be managed.

1. Base Staking Rewards

The foundation of the stack is the yield generated by restaking ETH into a Liquid Staking Token (LST) like rETH or cbETH. This is the most transparent layer, sourced directly from Ethereum’s consensus layer. It pays out in two forms: validator rewards (the protocol fee share) and MEV (Maximal Extractable Value) generated by block proposers. This layer carries the lowest risk in the stack, primarily tied to the underlying LST provider’s operational security.

2. Restaking Rewards

The second layer is the premium generated by restaking that LST into EigenLayer. By committing staked ETH to act as shared security for Actively Validated Services (AVSs), LRTs earn additional yield. This is the primary differentiator between LSTs and LRTs. However, this yield is not guaranteed; it depends on the demand for AVS security and the specific contracts used. This layer introduces smart contract risk and the unique "slashing" risks associated with the new AVS protocols.

3. Points and Incentives

The final layer consists of points, airdrop eligibility, and protocol-specific incentives. These are speculative rewards designed to bootstrap liquidity and attract early users. While they can significantly boost short-term returns, they are highly volatile and subject to change based on protocol governance decisions. This layer represents the highest risk, as points can be devalued or removed entirely without warning.

The risk-return choices that change the plan

Understanding this stack is critical for risk assessment. The base staking yield is relatively stable and predictable. Restaking yields are variable and tied to the success of the AVS ecosystem. Points and incentives are speculative and can disappear overnight. When analyzing an LRT, always break down the APY into these three components to see where the return is actually coming from and what risks you are assuming to get it.

Infrastructure Risks in Liquid Restaking

Liquid restaking tokens (LRTs) abstract the complexity of restaking, but they do not eliminate the underlying technical risks. In fact, they introduce a new layer of counterparty and smart contract exposure that investors must understand before allocating capital. The "yield" you see is often a reflection of these embedded structural vulnerabilities.

Smart Contract Complexity and Attack Surface

LRT protocols sit between the base layer (like Ethereum) and restaking networks (like EigenLayer). This intermediary position creates a larger attack surface than simple staking. Every additional smart contract layer—such as the LRT wrapper, the oracle feeding price data, and the governance module—introduces potential points of failure.

A vulnerability in any one of these contracts can lead to total loss of funds, not just the staking yield. For example, if the oracle fails to update the price of the underlying asset correctly, the LRT could be mispriced, leading to liquidations or arbitrage losses that drain the protocol's reserves. The complexity is not just code; it is the interaction between multiple protocols. A failure in the underlying restaking protocol can cascade through the LRT wrapper, as seen in various historical exploits where "safe" abstractions became the primary vector for hacks.

Withdrawal Queue Delays and Liquidity Mismatch

Perhaps the most tangible risk for LRT holders is the withdrawal queue. When you stake ETH directly, you can initiate a withdrawal, but it takes time to process. With LRTs, the situation is often worse. Many LRT protocols do not hold the underlying ETH in a way that allows for instant redemption. Instead, they rely on secondary markets or liquidity pools to provide exit liquidity.

During periods of market stress, this liquidity can dry up. You might hold an LRT token that is theoretically backed by ETH, but you cannot sell it at the expected rate. This creates a "liquidity mismatch" where the promise of liquidity does not match the reality of the underlying infrastructure. In extreme cases, protocols have implemented "withdrawal queues" that can delay access to your funds for weeks or even months, effectively locking your capital during the very time you might need it most.

The Gauntlet Framework Perspective

Industry analysts, such as those at Gauntlet, have developed risk frameworks specifically to evaluate these LRT-specific vulnerabilities. Their analysis highlights that the risk is not static; it evolves as the protocol scales and integrates with new restaking networks. The key takeaway is that LRT yield is not free money—it is a premium for accepting these specific infrastructure risks. Understanding the depth of the withdrawal queues and the robustness of the smart contract audits is essential for any serious assessment of LRT viability.

Comparing top LRT protocols

Use this section to make the LRT Yield Analysis decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Evaluating yield sustainability

LRT Yield Analysis works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

LRT Investment Checklist

Before allocating capital to a Liquid Restaking Token, treat your due diligence as a stress test, not a purchase. LRTs layer multiple protocols, which amplifies yield but also compounds failure modes. Use this checklist to verify the structural integrity of the protocol before you commit.

Confirm which consensus layer the LRT interacts with (e.g., Ethereum, Solana) and which validator set it delegates to. Check if the protocol uses a decentralized oracle network or a single centralized provider for price feeds. A single point of failure in the oracle can lead to incorrect liquidations or yield calculations.

Review the audit reports from reputable firms like OpenZeppelin or Trail of Bits. Pay attention to the severity of any findings and whether they have been fully patched. Look for the presence of a bug bounty program, which indicates ongoing security vigilance. Check if the contract has a timelock on upgrades to prevent sudden, malicious changes.

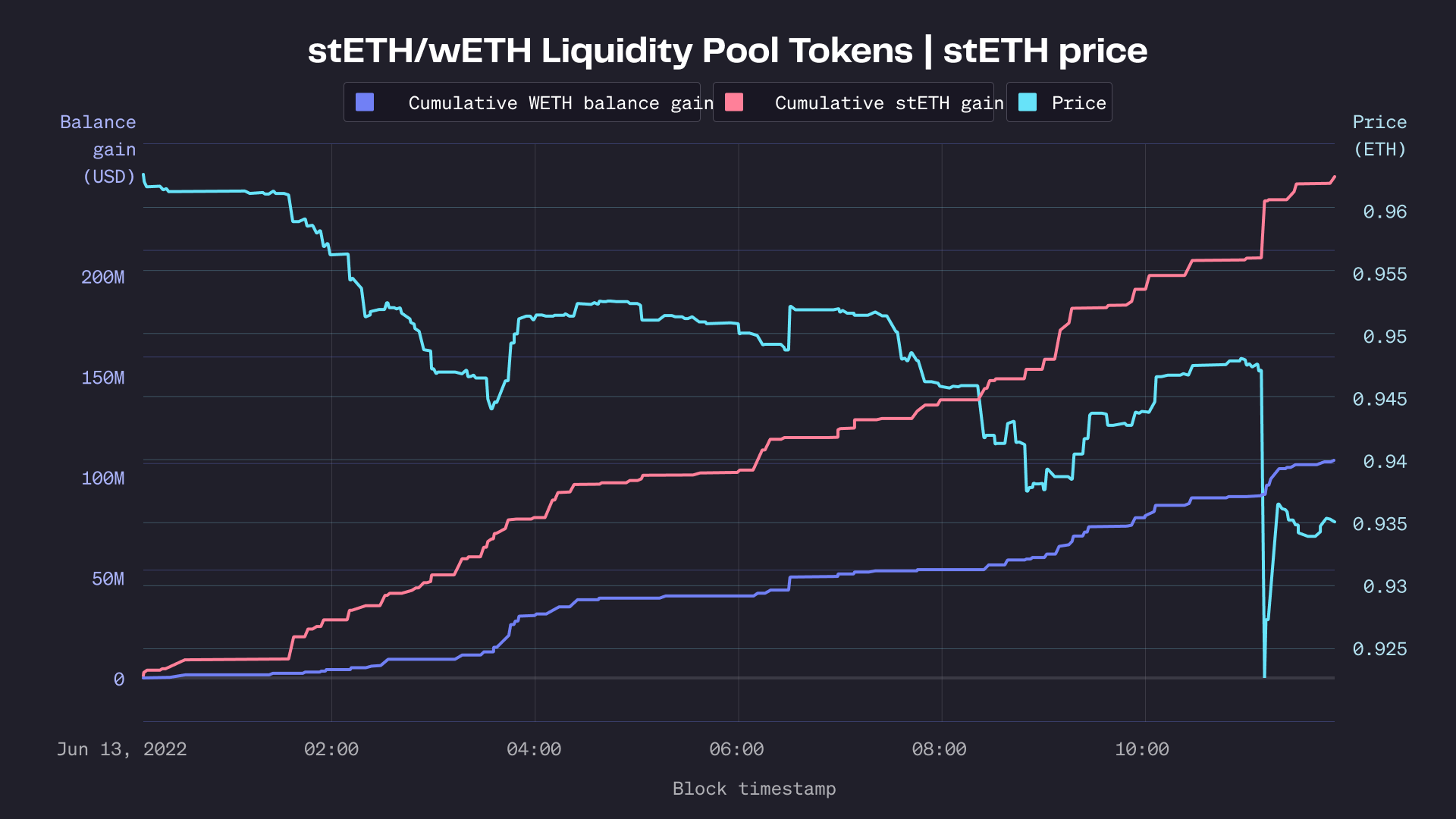

Analyze the historical volatility of the LRT against its underlying asset. Use a provider-backed chart to visualize drawdowns during market stress. If the LRT trades at a significant discount to its underlying asset, understand the reason: is it a liquidity issue or a fundamental flaw in the redemption mechanism?

Be skeptical of yields that appear too good to be true. Determine the source of the yield: is it from base staking rewards, restaking incentives, or protocol subsidies? Subsidies are often temporary and can disappear, causing the yield to collapse. Look for protocols that generate yield from real economic activity rather than token emissions.

Ensure there is sufficient liquidity on decentralized exchanges to exit your position without significant slippage. Check the depth of the liquidity pools and the presence of impermanent loss protection. In a crisis, high liquidity is the only thing that allows you to exit safely.

The chart above shows the volatility of the underlying asset. Use this as a baseline; LRTs often exhibit higher volatility due to the additional layers of risk. If the underlying asset is stable, the LRT's volatility likely comes from smart contract or oracle risks. If the underlying asset is volatile, the LRT amplifies that risk. Always assume the worst-case scenario when modeling your returns.

No comments yet. Be the first to share your thoughts!